We face 'extraordinary' times, 'very sensitive' times, international headwinds and fragility. But the overarching message we are meant to take away from this year's Budget with is a positive one.

In his 2016-17 Budget speech, delivered tonight, Australian Treasurer Scott Morrison stated that the Turnbull Government understands the economic challenges Australia faces. And indeed there is a comprehensive range of measures and policy announcements intended to assure us that the government is responding to our challenges and successfully navigating the transition away from the mining boom.

Unfortunately, the Treasurer's words have been undermined somewhat by his extremely light treatment of the global challenges and risks that are materially important to the Budget figures.

The avoidance of international context is particularly worrying on the back of the Treasurer's decisions not to attend the IMF, World Bank and G20 meetings in Lima last October and in Washington last month, as well as other recent international gatherings.

The scant international content in the Treasurer's remarks is particularly striking in light of the 0.25% interest rate cut announced this morning by Reserve Bank of Australia Governor Glenn Stevens. In justifying the interest rate decision, the key factors cited by the Reserve Bank Board were primarily global in nature. Weighing on the Board was a confluence of downgrades in global economic forecasts, uncertainty about the economic outlook, difficult conditions in emerging-market economies, and the divergence in monetary policy settings.

The Treasurer cited precisely none of these factors in his speech.

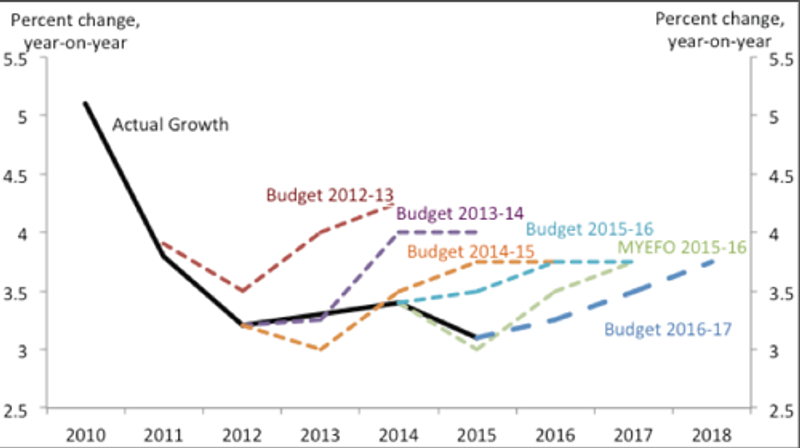

He had much to work with. Digging into the details of the Budget papers suggests a prudent, middle-of-the-road set of estimates about the global economy, awareness of the risks, and broad alignment with the international economic discourse and the Reserve Bank Board decision.

The US, Japan and Euro area are expected to grow at modest rates or remain subdued out to 2018 the forecast years. As for our emerging-market trading partners, the ongoing Chinese transition means moderating growth and ongoing risk to the global economy, India's title as fastest growing major country in the world will continue to present opportunities, and other East Asian countries are expected to grow slowly relative to history.

The overall picture is one of moderating global growth, reflecting unresolved crisis legacies, low productivity growth and unfavourable demographics. [fold]